4

4 0

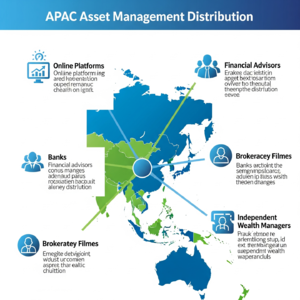

0Distribution Channels

Asset managers in APAC (ex-Japan, ex-India) utilize various channels to reach investors, often employing a multi-channel approach tailored to specific markets and client types.

Key distribution channels include:

•

Banks: Banks remain the dominant force in fund distribution across many APAC markets due to their extensive branch networks, large customer bases, and established trust. In Taiwan, banks hold a 55% share of fund sales volume, while in Thailand, the banking channel accounts for 67% of mutual fund distribution. In Hong Kong and Singapore, banks control the majority of fund sales, around 55-60% and roughly 70% respectively, though this share has decreased slightly over the past decade in some markets. Mainland China's traditional bank dominance is evolving, but they remain primary distributors. Banks may distribute both their own asset management subsidiaries' products and third-party funds, leveraging open-architecture platforms. Gaining "shelf space" at major banks is critical for asset managers targeting the retail market.

•

Securities Firms and Brokerages: These are particularly prominent in markets like South Korea, where they have historically held the largest share of retail fund sales (around 56%) compared to banks (around 39%). Securities firms leverage their existing client base and often focus on HNW or active trading clients.

•

Insurance Companies: Insurance companies act as a distribution channel primarily through unit-linked policies and retirement plans. In Hong Kong, they comprise roughly 35% of retail fund sales, a share that has grown significantly. They use their captive client base and large agency forces, though pure investment platforms have impacted their growth in some markets. This channel is significant in Hong Kong and Singapore but relatively small in mainland China.

•

Independent Financial Advisors (IFAs) and Wealth Managers: While a minor channel in most APAC markets, IFAs offer tailored advice and a wider product selection, appealing particularly to HNW and mass affluent segments. Their growth can be influenced by regulations like the banning of commissions, as seen in Australia where the Future of Financial Advice (FoFA) reforms shifted distribution away from commission-based models. In Hong Kong, IFAs account for a small share (~2-3%).

•

Digital Platforms and Online Channels: This is a rapidly growing area, including direct-to-consumer platforms, robo-advisors, and online brokerages. These channels appeal to tech-savvy investors, facilitate access to lower-cost products like ETFs, and enhance accessibility and convenience. Mainland China is a leader in online fund distribution, with platforms like Alipay and WeChat accounting for a significant portion of sales (roughly 30-35%) and a corresponding decrease in banks' share. Australia also sees significant digital uptake. Digital channels are expected to play a major future role, particularly for younger, mass-market investors.

•

Asset Manager Direct Sales: While limited for retail, asset managers maintain internal sales teams focused on institutional and wholesale distribution, managing relationships with large clients and intermediaries like private banks, national distributors, and institutions. Some large managers offer direct online portals, but this is a minor channel compared to banks. The value lies more in B2B relationships with distributors than direct retail sales.

The distribution landscape is increasingly becoming omnichannel, with banks and traditional players integrating digital offerings to maintain their reach. Strategic partnerships between asset managers, banks, fintech firms, and platform providers are becoming more prevalent.